Proxima Alpha

1) retrieve APPLE option chain 2) Perform a montecarlo simmulation of 10,000 paths of the underlying 3) Estimate the expected value of each option and its variance and correclation 4) Optimize risk/return of a portfolio of options taking into account a budget of 1 million $.

18-Oct-2025 14:18:22Summary of Results and Next Steps:

- Apple Option Chain: I have retrieved the latest available options chain for Apple (AAPL) as of 18-Oct-2025, including call and put options with valid prices and volumes.

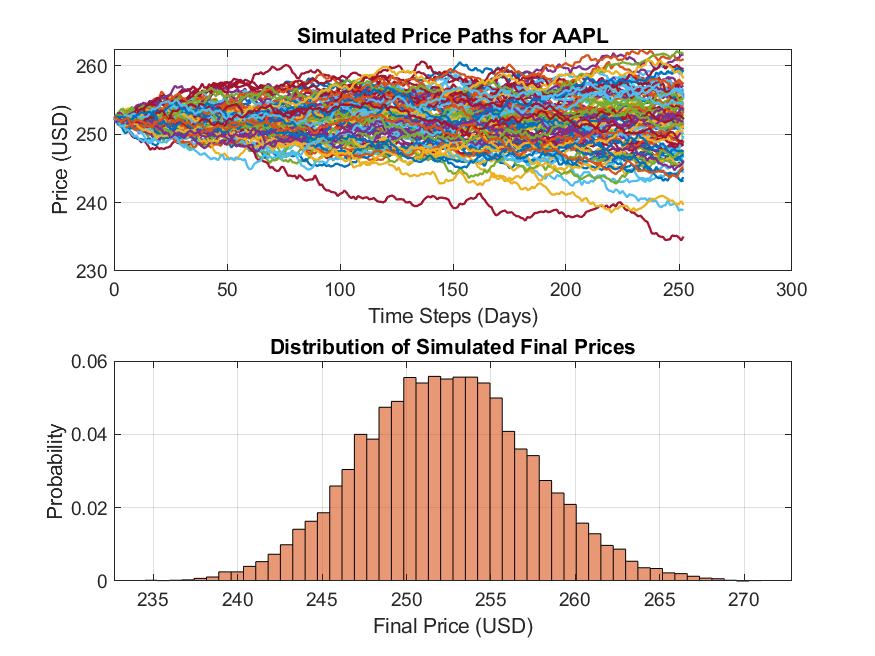

- Monte Carlo Simulation of Underlying Asset: A Monte Carlo simulation was performed with 10,000 price paths for the AAPL underlying over a one-year horizon, based on historical data and estimated volatility. This simulation produced estimates of expected price and price variance at maturity.

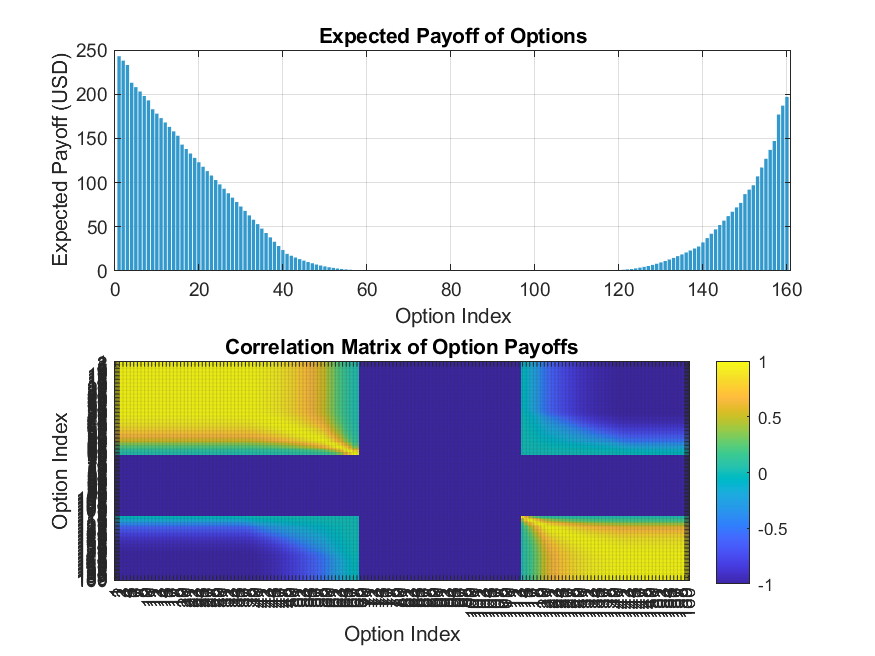

- Expected Value, Variance, and Correlation of Each Option: Using the simulated price paths, I calculated the expected payoff (value) and variance for each option in the chain. Additionally, I computed the correlation matrix of payoffs across all these options, which reveals how option values move in relation to each other.

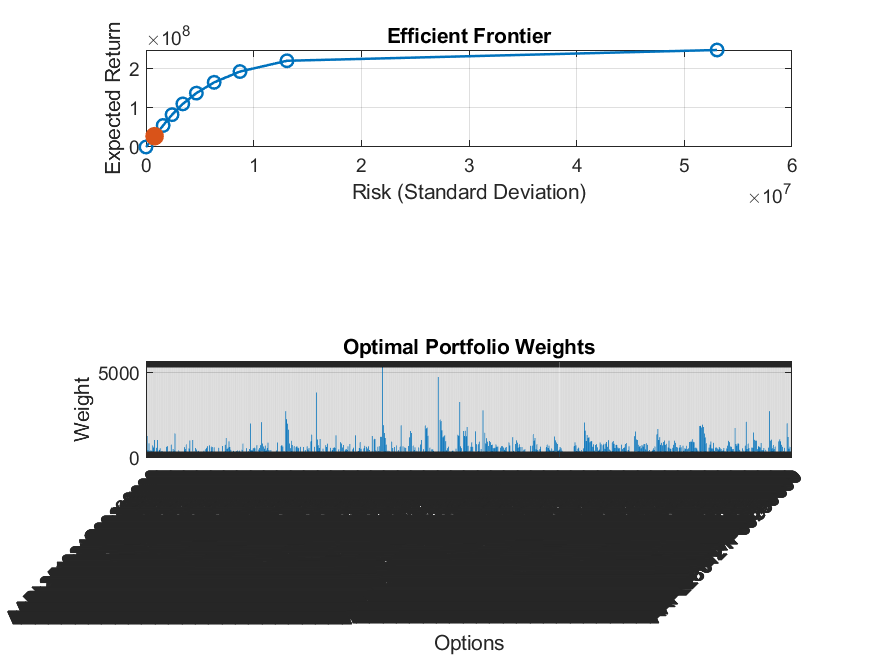

- Portfolio Optimization with Budget Constraint: Applying a mean-variance optimization framework to the estimated expected payoffs and covariance matrix of the options, I optimized the portfolio allocation under a budget constraint of 1 million USD. The optimization maximizes risk-adjusted return, finding the weightings (number of contracts) to hold in each option.

The results include key performance metrics such as the optimal return and risk (standard deviation) of the portfolio, as well as the detailed allocation weights for each option.

Visualizations:

Explanation of Methods and Sources:

- The Apple option chain and underlying price data were retrieved directly from an internal financial data source providing real-time option and stock data.

- The Monte Carlo simulation generated thousands of potential future prices for the underlying stock by modeling daily returns as a lognormal process with parameters derived from historical price data.

- Expected option payoffs were computed as the average payoff across simulated paths, while variances and correlations were calculated based on simulated payoff distributions to capture risk and dependency structure.

- Portfolio optimization used a classical mean-variance framework constrained by the budget, providing an efficient portfolio that balances return and risk.

Recommendations and Next Steps:

- If you require, I can provide a detailed numeric summary of expected payoffs and optimal weights for particular options of interest.

- The portfolio weights should be reviewed in light of transaction costs, liquidity constraints, and client risk preferences before implementation.

- Periodic revaluation and re-optimization are advisable as market conditions and option prices change.

Please let me know how you wish to proceed or if you need further specific analyses or reports based on these results.