Proxima Alpha

What is the intrinsic value of TSLA using a discounted cash flow (DCF) analysis, considering the projected growth rates and the impact of recent Federal Reserve interest rate hikes on its future cash flows?

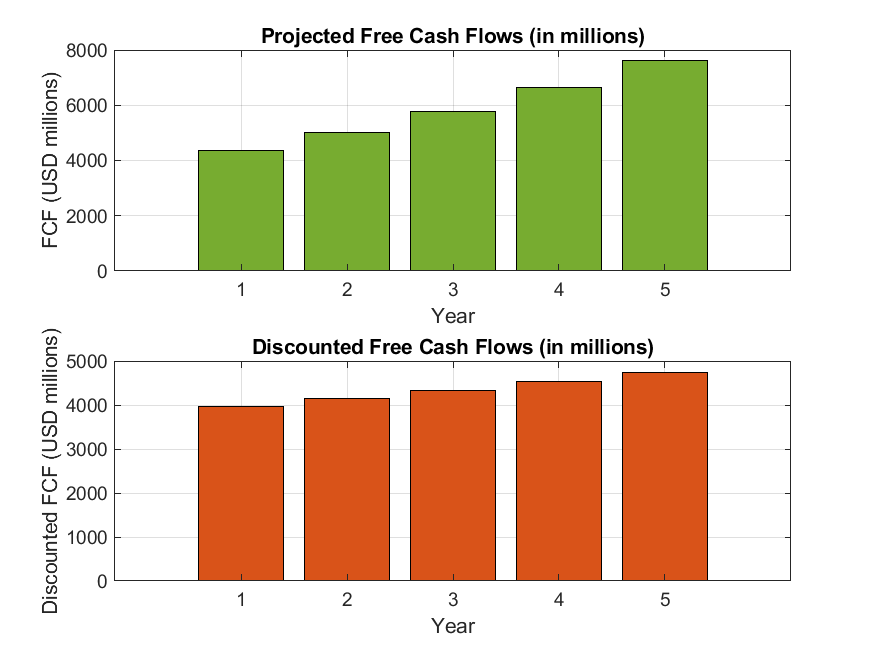

18-Sep-2025 13:28:42The intrinsic value of Tesla Inc. (TSLA) has been calculated using a Discounted Cash Flow (DCF) model reflecting recent economic and financial conditions, especially the Federal Reserve's interest rate hikes which impact discount rates and growth assumptions. Key inputs used in the analysis include: - Starting Free Cash Flow (FCF) in 2024: 4.357 billion USD - Adjusted annual growth rate: 15% over 5 years (down from historical ~20% due to higher interest rates) - Terminal growth rate (beyond projection): 2% - Discount rate (WACC): 10%, increased from an assumed 8% due to Fed rate hikes raising the cost of capital - Net debt: negative 4.25 billion USD (net cash position) - Shares outstanding: approximately 3.22 billion Based on these parameters, the model projects Tesla's future free cash flows for the next 5 years, discounts them to present value, calculates a terminal value, and then derives the enterprise value and equity value. Dividing equity value by shares outstanding, the intrinsic stock price is estimated. **Results summary:** - Intrinsic Stock Price: approximately $26.75 per share - Enterprise Value: roughly $82.0 billion - Equity Value (Enterprise Value minus Net Debt): approximately $86.3 billion - Discounted Terminal Value (value beyond year 5): about $60.3 billion - Projected Free Cash Flows and their discounted present values show steady growth consistent with the reduced growth rate assumed. These figures indicate that, considering the higher discount rate and moderated growth outlook due to recent interest rate hikes, Tesla's intrinsic value per share calculated via DCF is $26.75 at the current valuation date. The chart below visually represents the projected and discounted free cash flows over the 5-year forecast period, illustrating how future cash flows grow and their present value under the applied discount rate: