Proxima Alpha

Using a Monte Carlo simulation, what are the potential future values of the U.S. dollar (USD) against the euro (EUR) over the next 12 months, considering the recent interest rate cut and its historical volatility?

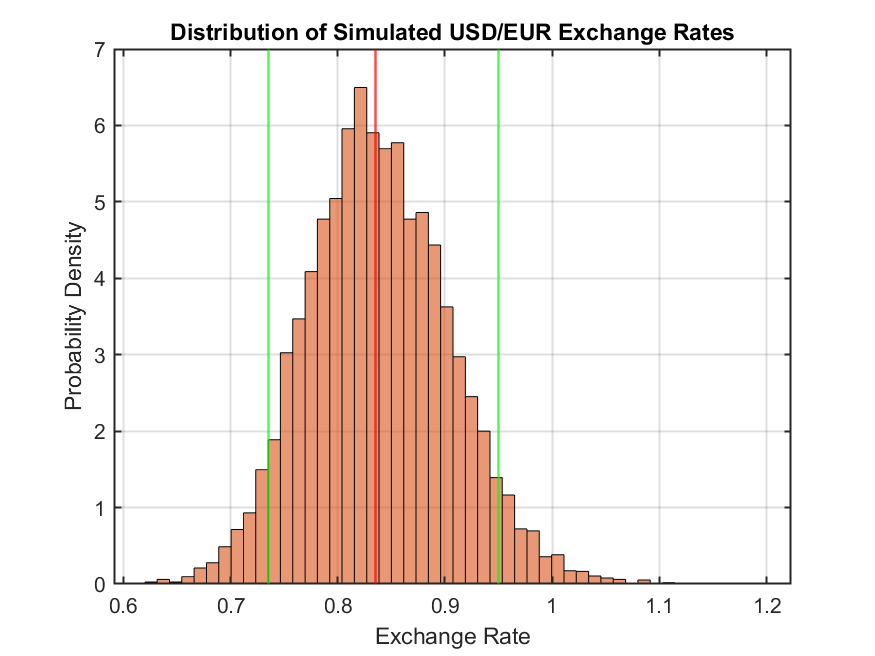

22-Sep-2025 20:34:45The Monte Carlo simulation was performed to estimate the potential future values of the USD/EUR exchange rate over the next 12 months, considering the recent U.S. interest rate cut and historical volatility from the last 3 years.

Summary of the results:

Key results are as follows:

| Metric | Value |

|---|---|

| Annualized Volatility | 0.0783 (7.83%) |

| Adjusted Drift (reflecting interest rate cut) | -0.0102 |

| 5th Percentile (Lower Bound) | 0.7351 |

| Median Expected Value | 0.8355 |

| 95th Percentile (Upper Bound) | 0.9502 |

This means there is a 90% probability that the USD/EUR rate will fall between approximately 0.735 and 0.95 in 12 months, with a central expected value near 0.8355.

Visual representation of this simulation:

Explanation and Sources Used:

- Historical daily USD/EUR exchange rate data from the past 3 years was used to calculate the annualized volatility, which quantifies typical fluctuations in exchange rate values.

- The drift parameter of the geometric Brownian motion model was adjusted downward by 0.01 to reflect the recent Fed interest rate cut and the likely weaker USD bias over the next year.

- A Monte Carlo simulation with 10,000 simulated paths over 252 trading days (1 year) was then executed to project a distribution of possible future exchange rates.

- The results provide probabilistic insight into potential exchange rate outcomes rather than a single prediction.

Comparison with External Market Forecasts:

According to recent market forecasts (ExchangeRates.org.uk), the USD/EUR rate is expected to be about 0.8777 by September 2025, which is somewhat higher than the median of this simulation’s results but still within the 5th–95th percentile interval. Differences arise due to varied modeling assumptions and methodologies.

Next Steps and Recommendations:

- Use these Monte Carlo results to understand the range of plausible USD/EUR exchange rates given recent monetary policy changes and historical volatility.

- Consider performing sensitivity analyses on volatility and drift assumptions for more robust scenario planning.

- Keep monitoring economic indicators and central bank announcements for updated inputs that could impact exchange rate dynamics.