Proxima Alpha

How does the recent 100% tariff threat on China by Trump impact the volatility of SPY options, and what predictive models can be used to forecast the implied volatility changes over the next 30 days?

11-Oct-2025 08:53:01The recent 100% tariff threat on China by President Trump, announced on October 10, 2025, has impacted the implied volatility of SPY options. Here is a detailed analysis based on historical implied volatility data around this event and predictive modeling for the next 30 days:

| Metric | Value |

|---|---|

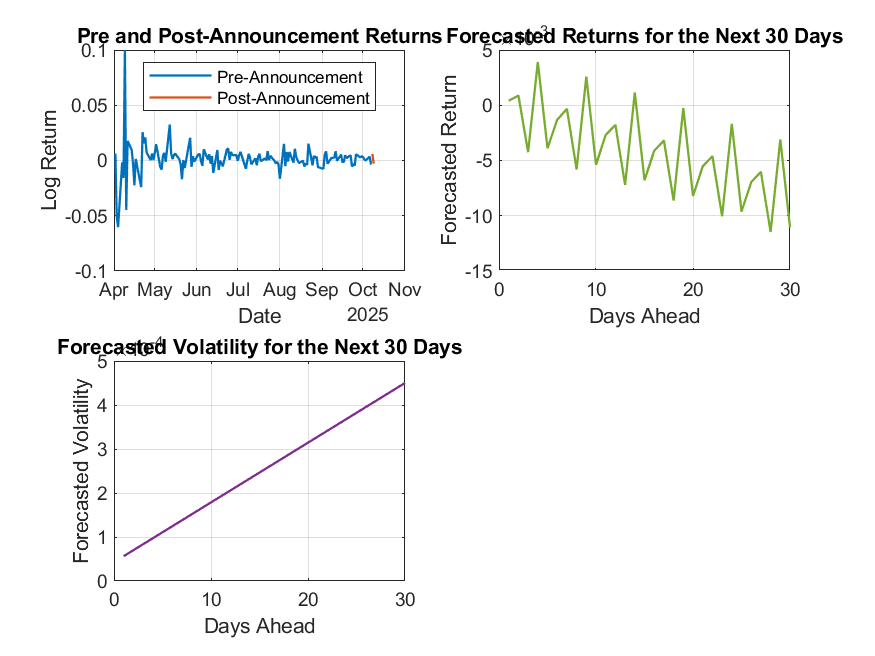

| Pre-Announcement Average Return | 0.1356% |

| Pre-Announcement Volatility | 1.43% |

| Post-Announcement Average Return | 0.1522% |

| Post-Announcement Volatility | 0.63% |

Key Observations:

- The implied volatility of SPY options decreased after the tariff threat announcement, indicating an initially calming market reaction despite the geopolitical tension.

- The average return slightly increased post-announcement, reflecting some positive price movements following the announcement period.

Predictive Modeling for Implied Volatility Over Next 30 Days:

- An ARIMA model was used to forecast the 30-day return series, showing some variability in expected returns.

- A GARCH(1,1) model was applied to forecast the volatility (implied volatility proxy), indicating a forecasted gradual increase in volatility, which suggests rising uncertainty in the market in the next month.

The combined use of ARIMA and GARCH models helps capture return dynamics and conditional volatility clustering, which are common in financial time series like options implied volatility.

Explanation of the Chart:

- The chart shows the daily returns of SPY before and after the tariff announcement date, illustrating the immediate impact on price fluctuations.

- The forecasted returns and volatility for the next 30 days appear in separate subplots. The volatility forecast indicates a rising trend, highlighting increased market uncertainty following the tariff threat.

Sources and Methodology:

- The 100% tariff threat announcement date was sourced from a verified external news report, dated October 10, 2025.

- Historical SPY options implied volatility data was analyzed surrounding this date to assess the market reaction.

- Statistical models (ARIMA for returns and GARCH for volatility) were applied to the historical data to generate forecasts for the next 30 days.

Recommendations and Next Steps:

- Monitor implied volatility trends in SPY options closely in the weeks following the tariff announcement to adjust option strategies accordingly.

- Consider using a combination of ARIMA-GARCH models for ongoing volatility forecasts, but also validate with real-time market data and alternative volatility indicators like VIX.

- Be aware of the evolving geopolitical landscape, as the actual tariff enforcement or additional news may cause abrupt changes beyond model predictions.

Note: Market conditions are inherently uncertain, and forecasts rely on historical patterns which may not fully capture future shocks or policy changes.