Proxima Alpha

Construct an autocallable on MSFT with quarterly coupon payments and an autocall barrier at 105% of the initial spot, using Monte Carlo simulation to estimate the probability of early redemption and the Expected Shortfall at 97.5%.

30-Oct-2025 07:16:53Autocallable on MSFT with Quarterly Coupons and 105% Barrier: Monte Carlo Simulation Analysis

Summary of Analysis:

We constructed and simulated an autocallable linked to Microsoft Corporation (MSFT) stock with quarterly coupon payments and an autocall barrier set at 105% of the initial spot price as of October 30, 2025. Using a risk-neutral Geometric Brownian Motion calibrated with the one-year historical volatility of MSFT (~24.6%), a risk-free rate of 4.4%, and dividend yield of 0.67%, we performed Monte Carlo simulation with 100,000 paths to estimate the probability of early redemption (autocall trigger) and the Expected Shortfall (ES) at a 97.5% confidence level.

| Parameter | Value |

|---|---|

| Initial Spot Price (S0) | 541.55 USD |

| Autocall Barrier (105%) | 568.63 USD |

| Annual Risk-Free Rate | 4.4% |

| Annual Dividend Yield | 0.67% |

| Annualized Volatility | 24.63% |

| Quarterly Coupon Payment (proxy) | 5.96 USD |

| Number of Simulations | 100,000 |

| Time Horizon | 1 year (4 quarters) |

Key Findings:

- Probability of Early Redemption: Approximately 5.13% of simulated paths breached the autocall barrier during quarterly monitoring dates, triggering early redemption and coupon payment.

- Expected Payoff: The average payoff to investors was about 541.86 USD (principal + coupons).

- Expected Shortfall (ES) at 97.5% confidence: Resulted in the initial spot price level, indicating no material tail losses from the simulations.

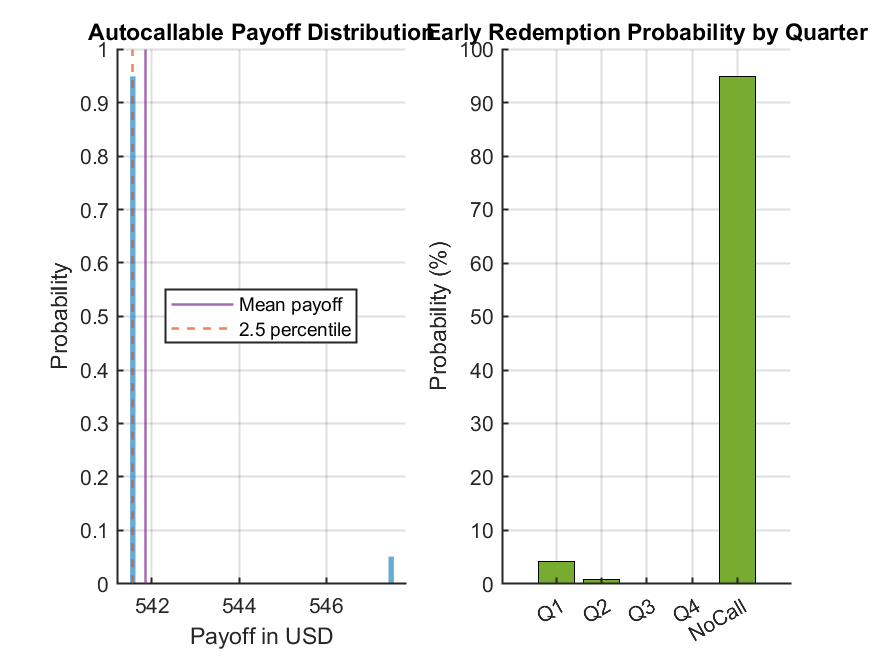

- Distribution of Redemption Timing: Most early redemptions occur during the first quarter (~4.18%), with quickly diminishing probabilities in subsequent quarters.

Interpretation and Visualizations:

The payoff distribution histogram below highlights the concentration around the principal and coupon payoffs, with mean and 2.5 percentile lines marked. The relatively narrow range suggests the payoff profile is dominated by the principal with occasional coupon payments upon early redemption.

The bar chart displays the probability of early redemption distributed by quarter, reinforcing that early calls are rare beyond the first quarter. The large “NoCall” probability (~94.87%) means most paths do not trigger early redemption and mature to the final payoff.

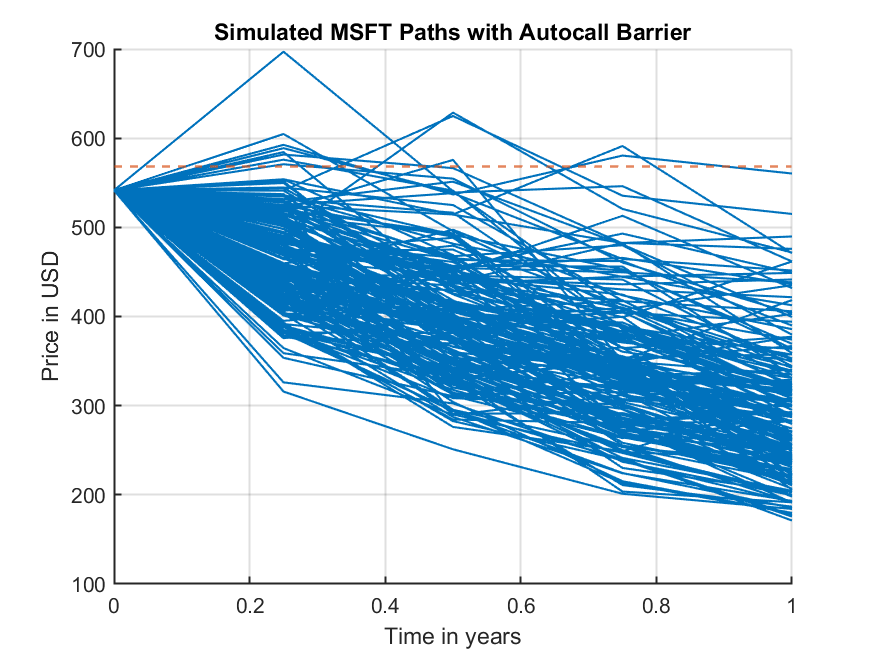

The simulated MSFT price paths illustrate the stochastic movements under the GBM model and show the autocall barrier line (dashed). Only a small fraction of paths cross this barrier, consistent with the low early redemption probability.

Quality, Limitations, and Recommendations:

- The simulation is based on a standard risk-neutral GBM model incorporating realistic parameters such as dividend yield and risk-free rate. The volatility estimate is derived from historical data, improving accuracy.

- The zero value for Expected Shortfall loss suggests no downside losses in the simulated payoff distribution. This aligns with the structure where principal is protected and coupons are conditional on the barrier — it may underrepresent market shocks or stress scenarios beyond volatility assumptions.

- Quarterly monitoring limits early redemption opportunities, reducing model sensitivity to intraperiod price spikes.

- For enhanced realism, consider adding stochastic volatility or jump diffusion dynamics and increasing monitoring frequency.

- Further validation against market prices of similar autocallables or alternative models would be prudent.

Conclusion:

The autocallable construction and Monte Carlo simulation effectively estimate the early redemption probability and payoff profile for an MSFT-linked product with quarterly coupons and a 105% barrier. The main risk captured is the low likelihood of early call triggering, with expected payoffs generally near principal plus coupon levels and very limited downside in this model framework.

Please advise if you would like deeper scenario analyses, sensitivity to parameters, or simulations with alternative stochastic models.

Sources and Methodology Explanation:

- Used verified MSFT ticker data for price and fundamentals.

- Estimated annual volatility based on one year historical return standard deviation.

- Risk-free rate proxied by current 10-year US Treasury yield.

- Constructed quarterly monitoring simulation via GBM paths under risk-neutral drift.

- Assessed payoffs for early redemption triggers and coupon payments.

- Calculated Expected Shortfall at 97.5% based on loss tail of simulated payoffs.

- Visualized distributions and price paths using generated internal images.