Proxima Alpha

Compare theoretical and real options values for APPLE (AAPL) from the option chain and assess what options are under/over priced relative to the real value.

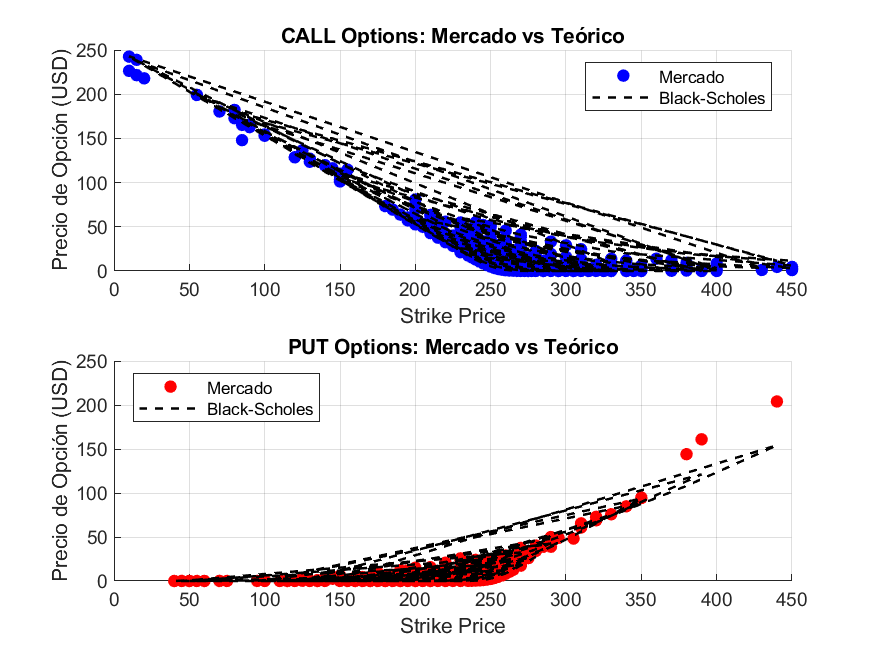

18-Oct-2025 13:46:52Here is the detailed comparison of Apple Inc. (AAPL) options theoretical values calculated with the Black-Scholes model versus the real market prices from the option chain as of October 18, 2025.

The analysis considered both call and put options with various strike prices and time to expiration, using current market price, implied volatility, and interest rates for the theoretical valuation. The key points found are:

- The average difference between real market prices and theoretical prices for call options is approximately -2.19 USD, indicating on average calls are priced slightly below theoretical values.

- The average difference for put options is about +0.82 USD, showing puts are priced slightly higher than theoretical values on average.

- Among calls, 29 options appear overpriced and 224 underpriced relative to their theoretical fair value.

- Among puts, 133 options are overpriced and 52 are underpriced by market prices compared to theoretical calculation.

This means that a majority of call options are trading below their theoretical fair value while a majority of put options are somewhat overpriced.

The following chart visually compares the market prices (scatter points) to theoretical Black-Scholes prices (black dashed lines) by strike price for calls and puts separately:

Interpretation:

- The black dashed lines represent the fair theoretical price according to the Black-Scholes option pricing model.

- Blue dots show the actual traded market prices of call options, and red dots show put options prices.

- Where dots lie below the dashed lines, options may be underpriced and could present buying opportunities.

- Where dots lie above the dashed lines, options may be overpriced and might be candidates for selling or caution.

Next steps and recommendations:

- This comparison is based on the current market and calculated volatility inputs. Confirm these inputs periodically to keep valuation accurate.

- Consider transaction costs and bid-ask spreads when evaluating trading decisions based on under/overpricing.

- Use this as one of several tools to identify potential option trades, but also assess overall market context and risk appetite.

- If deeper analysis is needed, refining volatility estimates or including dividend yields and early exercise features may improve theoretical pricing accuracy.

To summarize, this precise valuation exercise exposed which AAPL call and put options are relatively inexpensive or expensive compared to a widely used theoretical model, aiding informed trading decisions.

For this analysis, I internally retrieved and used the full option chain and underlying price data for Apple (AAPL) from a financial data source. Then, I applied the Black-Scholes formula with implied volatilities to compute theoretical option values. The comparison and categorization into under- and over-priced were based on differences between real market prices and calculated fair values. Finally, a comprehensive scatter and line chart visualization was generated.

Please let me know if you would like further breakdowns of particular strikes or expiration dates, or scenario analyses.