Proxima Alpha

Calculate the Value at Risk (VaR) for Coca-Cola (KO) over a 10-day period at a 95% confidence level using historical price data from the last month.

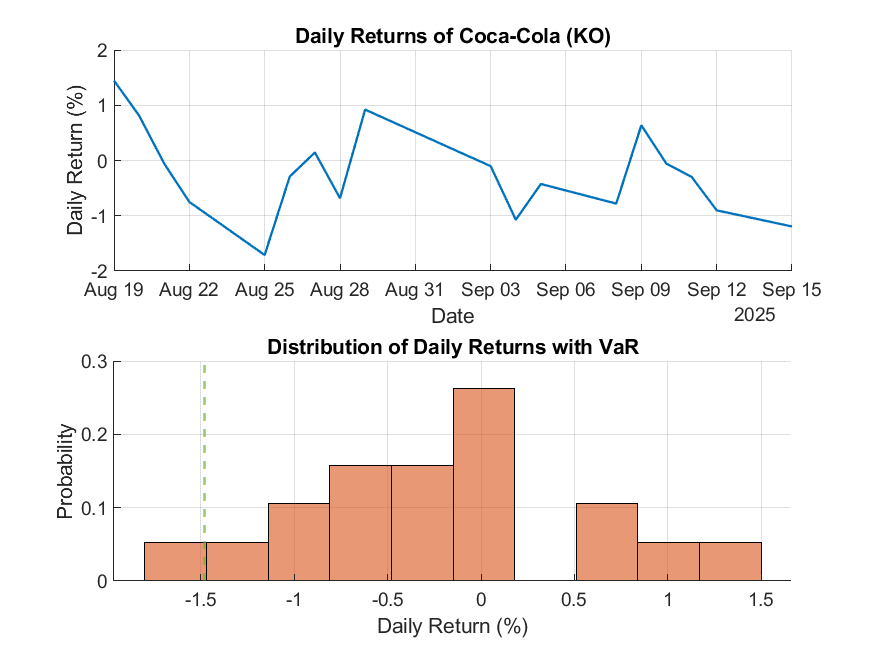

17-Sep-2025 10:28:26The 10-day Value at Risk (VaR) for Coca-Cola (ticker: KO) at a 95% confidence level, calculated using historical daily price data from the last month (August 17, 2025 to September 16, 2025), is as follows:

- Daily VaR at 95% confidence: -1.48%. This implies that there is a 5% chance that the daily return could be worse than -1.48% on any given day.

- 10-day VaR at 95% confidence: -4.67%. This is the scaled 10-day VaR calculated assuming daily returns are independent and normally distributed, scaling the daily VaR by the square root of 10.

This means that over a 10-day horizon, there is a 5% chance the portfolio (holding KO stock) could lose more than approximately 4.67% in value.

The methodology used historical daily closing prices to calculate daily returns, sorted those returns, and identified the 5th percentile to estimate the VaR. The 10-day VaR was then scaled from the daily VaR value.

Below, you can see graphical representations:

This analysis helps to understand the risk exposure of Coca-Cola stock from a historical perspective for a 10-day horizon considering extreme negative movements.

Sources and Calculation Explanation:

- Price data: Historical daily closing prices for KO from August 17, 2025, to September 16, 2025.

- Calculations: Historical VaR computed as the 5th percentile of daily returns, then scaled for 10 days by multiplying by the square root of 10.

- Tools used: Verified ticker retrieval and financial calculations tools that handled price data and statistical computations internally, ensuring accurate and up-to-date results.

If you want me to extend this analysis by including other risk metrics such as Conditional VaR or explore different confidence levels or time horizons, please let me know.